India–France Revised Double Taxation Avoidance Convention

Context

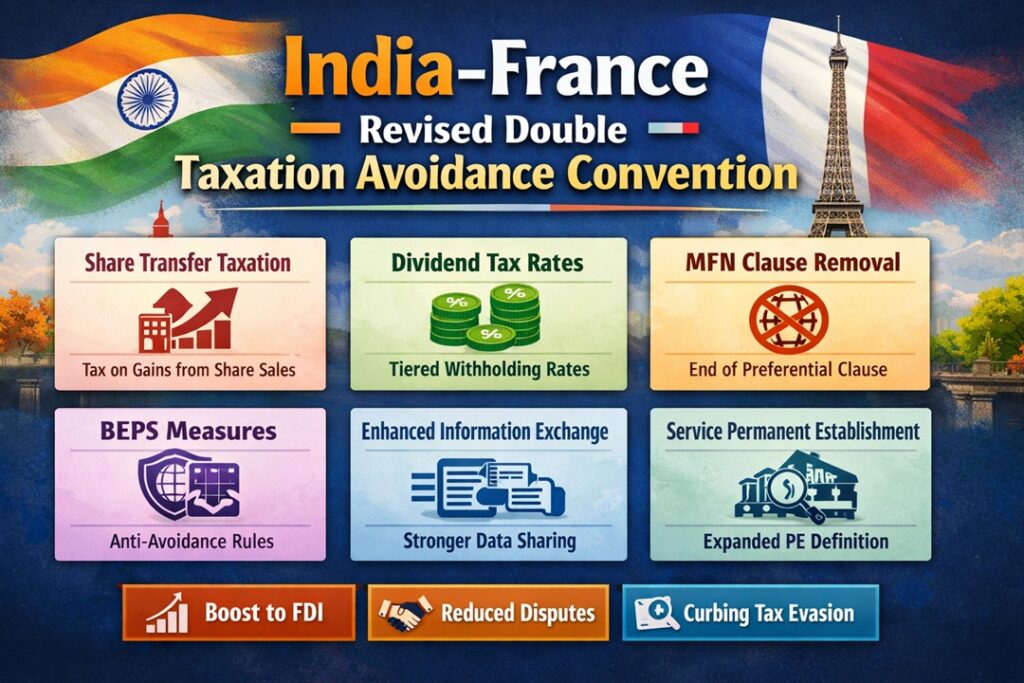

India and France have signed an Amending Protocol to update their 1992 bilateral tax treaty, ensuring consistency with contemporary international taxation standards.

Bilateral Tax Treaty: Core Idea

Meaning:

A Double Taxation Avoidance Convention is a reciprocal arrangement between two nations to prevent dual taxation of the same income in the source country and the country of residence.

Relief Framework:

Taxing powers are allocated according to income type, with relief granted through:

- Single-Jurisdiction Taxation: Income taxed exclusively in one country.

- Foreign Tax Credit System: Resident country allows credit for taxes paid abroad.

Salient Amendments under the India–France Protocol

Taxation of Share Transfers:

Assigns taxing authority on capital gains from share sales to the country where the company is resident.

Dividend Withholding Structure:

Introduces a differentiated rate regime based on the extent of shareholding.

Elimination of MFN Provision:

Removes the Most-Favoured-Nation clause, reducing interpretational uncertainty and treaty disputes.

Anti-Avoidance Alignment:

Adopts BEPS-oriented provisions through the Multilateral Instrument to counter treaty abuse.

Administrative Cooperation Upgrade:

Strengthens exchange of information mechanisms and enables assistance in tax collection.

Expanded Permanent Establishment Norms:

Broadens the PE concept by including service-based establishments and standardising treatment of technical service fees.

Implications

Investor Confidence:

Predictable tax rules enhance the attractiveness of India and France for cross-border investments.

Dispute Minimisation:

Clear allocation of taxing rights reduces litigation and interpretational conflicts.

Fiscal Transparency:

Improved cooperation supports detection of tax evasion and profit shifting.

Source : PIB